You might face some sudden bills when you are running a small business. One day things look fine, the next a big bill lands, or a client pays late. These moments can stop growth or even threaten your cash flow.

The quick loans bridge these gaps when banks move too slowly. They turn urgent money worries into solved problems within days, not weeks. Many can also get urgent business loans for bad credit.

Many new lenders look at your recent sales rather than past money troubles. They check how you’re doing now, not mistakes from years ago. Some offer second-chance terms with slightly higher rates but quick approval.

Benefits of Quick Business Loans

The quick business loans can be a real lifesaver for companies in the UK. Here are some benefits of these loans:

- You will have fast access to funds. Most lenders can get pounds into your account within 24-48 hours, letting you handle sudden costs without delay.

- They offer good terms that match your business cycle. You can often choose payment plans that match when money comes in, not rigid dates.

- A timely loan helps you grab chances that won’t wait, like buying discounted stock or taking on a big new client job.

- Your credit score increases if you stick to the payment plan. Your on-time payment shows other lenders you’re a safe bet for future funds.

- Most quick lenders want just basic details about your business, not the massive files that banks demand.

- Many quick loans are unsecured, keeping your personal stuff safe if things go wrong.

Types of Emergency Business Loans in the UK

Many business owners need to know their options. The right emergency funding can mean staying afloat during emergencies.

Short-term Loans

These loans are from a few weeks to about 18 months. You get a lump sum upfront and pay it back in set payments. The interest rates sit higher than bank loans but lower than some other quick options. They work best for one-off costs like fixing a broken gear or paying a sudden tax bill.

Merchant Cash Advance

This clever option takes a cut of your daily card sales. You get money now and pay back as you earn through customer payments. The cost comes as a factor rate rather than a normal interest. It fits shops and food spots that take lots of card payments every day.

Invoice Finance

If clients owe you money, why wait? Invoice finance lets you get up to 90% of the bill value right away. The lender takes a small fee, and you get cash to use now. This suits companies with big clients who pay slowly.

Overdrafts

An agreed overdraft gives you a safety net when your bank balance dips below zero. You only pay for what you use, making it cheaper than fixed loans for small gaps. Many online banks now offer this with less fuss than old high street banks.

| Loan Type | Description | Typical Approval Time | Repayment Term |

| Short-term loans | Quick funds for urgent costs | 24–48 hours | 1–12 months |

| Merchant cash advance | Based on future sales revenue | 1–2 days | Flexible |

| Invoice finance | Use unpaid invoices as collateral | 1–3 days | 1–12 months |

| Overdraft | Flexible small cash buffer | Same day | On demand |

Short-term business finance brokers can save you loads of time when cash needs hit. They know which lenders match your spot and which to avoid. The brokers check dozens of options in one go, often find better rates than you would alone, and handle most of the boring paperwork. They also explain tricky loan terms in plain talk.

How to Apply for Emergency Loans?

You do not want to deal with a lengthy process of issuing loans when your business needs money. It has been simplified by most of the best lenders. The following is a way to raise money fast:

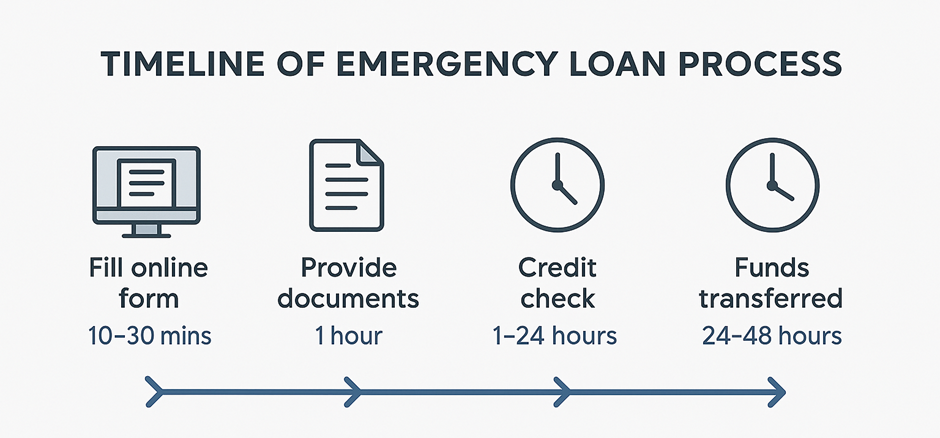

Step 1: Check what you need first: Gather your last six months of bank statements before you start. Have your company number, VAT details and tax info close by. Most lenders want to see proof you’ve been trading for at least six months with steady sales.

Step 2: Find the right lender match: Don’t just grab the first offer you see. Take an hour to check what fits your needs. Some lenders work best for shops, others for service firms. You can compare at least three options.

Step 3: Fill out the form carefully: Most online forms take under 15 minutes if you have your papers ready. You answer each question briefly and honestly.

Step 4: Send clear copies of papers: Take sharp photos of your ID, proof of address and bank pages.

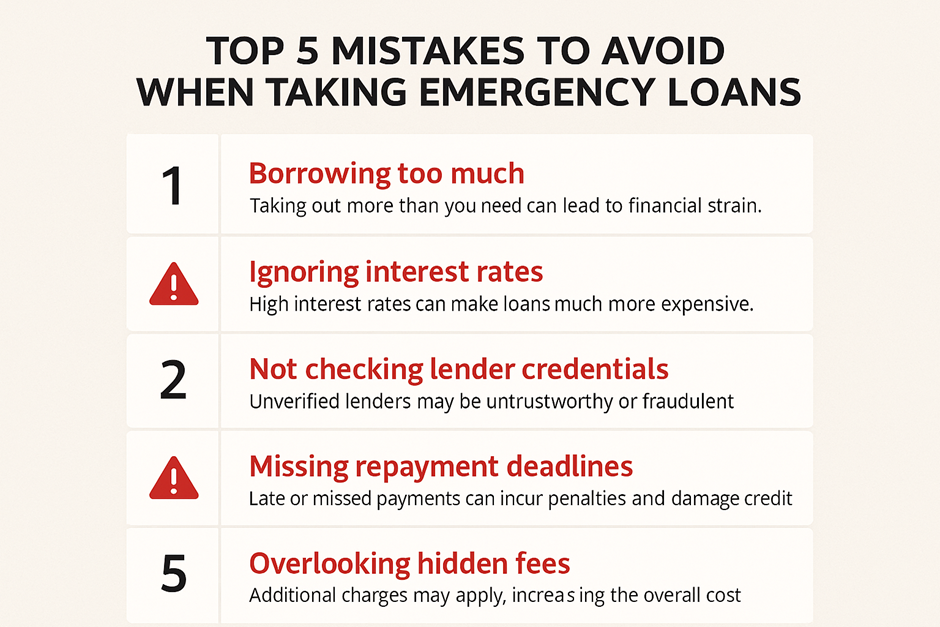

Step 5: Watch your phone and email: Once you hit send, keep your phone close. Most lenders call to check a few facts before saying yes. They might ask about recent big sales or drops in your account.

Who Can Get Emergency Business Loans?

These days, emergency cash isn’t just for established companies with perfect books. The lending market has grown far more welcoming to all sorts of business needs.

Start-ups with just six months of trading can now find options when cash runs tight. Many new lenders look at your recent sales trend rather than your years of accounts. They understand young firms often hit growth costs before they’ve built up savings.

The small shops can borrow these loans in case of roof leakages or refrigerator breakages. The costs of repairs cannot wait, and the funding will not have to wait either. The lenders have provided avenues through which companies with less than 5,000 monthly turnover can borrow funds within a short time. They review your actual bank flow rather than your credit scores.

Unpaid bills can unlock cash in the present day, when companies are waiting to receive large payments from clients. When you have sound but slow customers, lenders will find importance in such forthcoming payments. The invoice in itself serves as the collateral for your loan application. This goes even in situations when your own credit has a few dents.

Seasonal businesses like beach cafes or Christmas shops face unique cash gaps. Smart lenders now look at your whole year’s pattern, not just last month. They can offer terms that match your busy and quiet times with payments that flex when sales do.

Conclusion

You are aware of what to do in the event of an emergency. The emergency business loans are that much-needed breathing space when money is tight. The most successful companies take such loans not as a final solution but as a method to carry on their process. Your crisis can be like any other business challenge that has been solved tomorrow by the right lender match.

Harry Kane is a financial writer and author who has covered wide topics related to business loans and finance for the last decade. He has been working as the Chief Contributor in finding out deals on various business finance products covered by Thebusinessfunds, a reputed business loan broker firm in the UK. The primary work of Harry is to analyse the loan requirements of various businesses according to their circumstances and affordability. He directly communicates with the loan aspirants and guides them to get the right loan matching their needs. He has a vast experience in finance writing, working with many major business firms in the UK. At Thebusinessfunds, Harry also used to write well-researched blogs covering the financial problems of business loan aspirants and providing relevant solutions. He is a postgraduate with MSc. in Banking and Finance.