Limited companies face tougher money problems than sole traders do. Cash flow issues hit harder when you have staff wages. Monthly costs like rent and bills demand payment no matter what the sales. Seasonal firms struggle most when income goes up and down all year. Money pressure builds when bills arrive before customer payments come in.

Company directors worry about paying staff every single month without fail. Suppliers expect payment within thirty days, while customers pay much more slowly. Stock purchases need upfront cash, but sales happen weeks later. Cash problems force companies to turn down good new orders. Many good firms fail simply because money runs out for short periods.

Quick Access to Company Funding

Modern lending websites approve company forms within hours rather than weeks. Online systems process documents faster than old bank branch visits. Digital forms save time for busy company directors managing daily work.

Business loans for a limited company provide flexible terms that match trading. Companies can choose payment schedules that suit their specific cash flow. Seasonal payment options help companies manage quiet trading periods each year. Fixed rates protect companies from interest rate rises during the loan terms. Expert advice helps directors choose the right products for their needs.

Maintain complete control over the business

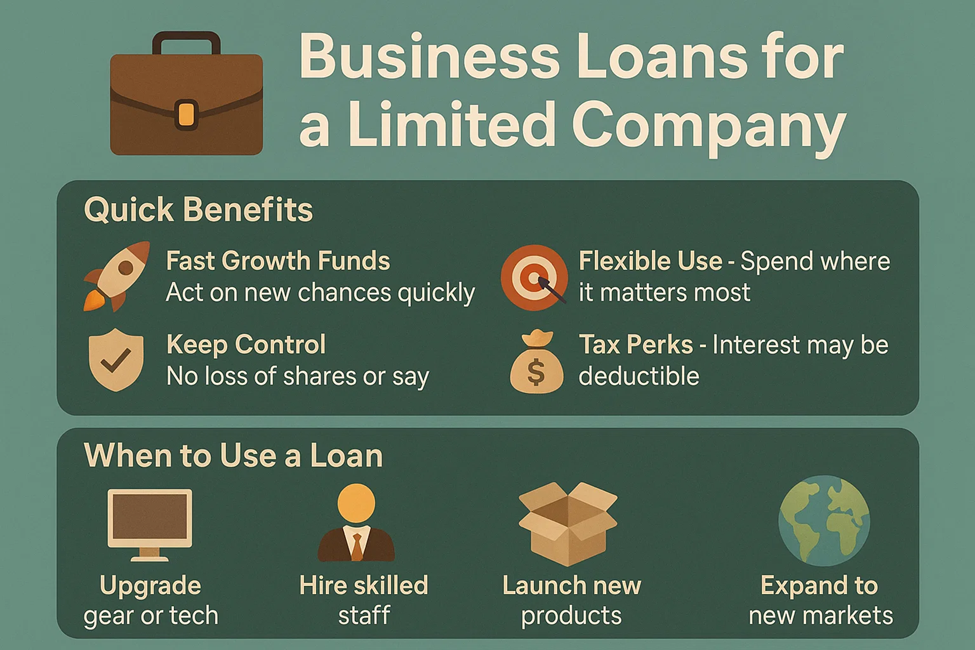

Business loans allow business owners to maintain complete control over their companies. In contrast to equity finance, you don’t relinquish any shares to investors. All company decisions remain with the initial directors and shareholders entirely. Voting rights remain unchanged as it was before taking any loan. The ownership of the company never gets altered when you take a loan instead.

- No surrendering of shares or votes

- The owner continues to make all of the decisions

- Business direction is always under your control

- Rapid decisions without investors’ approval

Flexibility in using the funds

Business loans are far more flexible compared to most other funding sources. Most lenders are concerned about your repayment capability, not how you spend. You are free to spend loan funds on inventory, machinery, personnel, or advertising. Cash flow issues are addressed when you spend funds where they are needed. Most loan products are free of restrictions on money.

- May be utilised for inventory, equipment, personnel, or advertising

- A lender usually does not place restrictions on spending

- Easy to match funds to business objectives

- Make a quick response to market opportunities

- Marketing campaigns during the best times

Build a good credit history

Having a good payment history on business loans enhances the credit score of your business. On-time monthly payments indicate to lenders that you handle money smartly regularly—credit scores lead to good deals and reasonable rates. A good credit record facilitates borrowing in the future for growth. Most successful businesses establish themselves through prudent borrowing and repayment.

Best business loan broker in the UK services assist businesses in obtaining appropriate deals. Skilled brokers understand which lenders have the best terms for various. Your credit rating will recover quickly if you select appropriate loan products. Expert consultation helps you make the correct loan selection based on careful assessment of repayment capacity. Reputable brokers save time and prevent expensive borrowing errors.

| Loan Type | Loan Amount | Loan Term | APR Range |

| Short-Term Loan | £5,000 – £50,000 | 3 – 18 months | 7% – 25% |

| Medium-Term Loan | £10,000 – £250,000 | 1 – 5 years | 6% – 18% |

| Unsecured Business Loan | £5,000 – £100,000 | 1 – 3 years | 8% – 22% |

| Secured Business Loan | £25,000 – £500,000+ | 2 – 10 years | 4% – 12% |

- Early repayments raise credit score

- Paves the way for larger loans in future

- More favourable terms and reduced charges

- Borrowing in the future becomes more convenient

- Adequate products are found by professional brokers

Tax benefits on interest

Business loan interest is usually an allowable tax-deductible business expense. This saves your firm’s tax bill and reduces borrowing costs considerably. Your accountants can indicate precisely which interest payments are relieved.

Tax saving renders business loans cheaper than borrowing for private purposes. Clever businesses utilise these advantages to minimise their overall financing cost.

- Leaves more cash for growth plans

- Effective borrowing rate drops with relief

- Professional accounting advice maximises benefits

- Tax-efficient strategies improve performance

Conclusion

Company growth needs money for staff and tools before profits increase. Growth projects need money for premises and initial setup costs early. Marketing campaigns need upfront spending before any sales results become visible.

New product work costs money months before revenue starts flowing in. Smart borrowing lets companies grow faster than other firms using profits alone.

Frequently Asked Questions (FAQs)

Who is eligible to apply for a business loan as a limited company?

Most limited companies will be eligible if they are actively trading and receive regular cash. Directors should typically have good credit records, and the company must have been in business for at least six months.

What documents are required for a limited company to apply for a business loan?

You need the director’s accounts for the last two years and bank statements. Most lenders also ask you to provide your business plan and proof of who the director is.

What types of business loans are available to limited companies?

Working capital loans are used to fund routine expenditure, and equipment finance to purchase new equipment. You can also obtain overdrafts, invoice finance, and commercial mortgages to purchase property.

How much can a limited company borrow?

Almost all businesses can borrow anything from £1,000 to £500,000, depending on how much you are earning annually. Most lenders lend you two or three times your annual income.

Can a startup limited company get a business loan?

New businesses have it more difficult, but lenders assist start-ups. You usually require a solid business plan and have to make personal guarantees.

Will I need collateral or a guarantor?

Smaller loans typically do not require any security, but larger loans typically require some assets. Personal guarantees of company loans are typically provided by directors, particularly for new companies.

Harry Kane is a financial writer and author who has covered wide topics related to business loans and finance for the last decade. He has been working as the Chief Contributor in finding out deals on various business finance products covered by Thebusinessfunds, a reputed business loan broker firm in the UK. The primary work of Harry is to analyse the loan requirements of various businesses according to their circumstances and affordability. He directly communicates with the loan aspirants and guides them to get the right loan matching their needs. He has a vast experience in finance writing, working with many major business firms in the UK. At Thebusinessfunds, Harry also used to write well-researched blogs covering the financial problems of business loan aspirants and providing relevant solutions. He is a postgraduate with MSc. in Banking and Finance.