Email:

Call:

Email:

Call:

You need to pay your VAT bill on time as it is a legal requirement. However, it is not easy to manage. Paying the quarterly bill halts the progress of your cash flow, especially in the off-season. And every pound is important when you are busy with growth investment.

A VAT loan in the UK could be the potential solution to manage a short-term burden without putting your HMRC record at risk. The loan is a strategic financial source tailored to bridge the gap and turn a burdensome lump sum into affordable monthly instalments.

At Thebusinessfunds, we help businesses in the UK to plan the Value Added Tax or VAT bill payment more effectively. We are well placed as the responsible commercial loan broker to explain how VAT loans work and match your business needs.

Commercial VAT loans are the specialised form of a short-term business loan. It is quite different from standard business finance, as the primary task is to manage the company's VAT obligation.

Here is how VAT loans function:

In a nutshell, you get relief by not paying one large lump sum to HMRC. Instead, you spread the cost over several monthly repayments. It helps you with cash flow management and manage your budget comfortably.

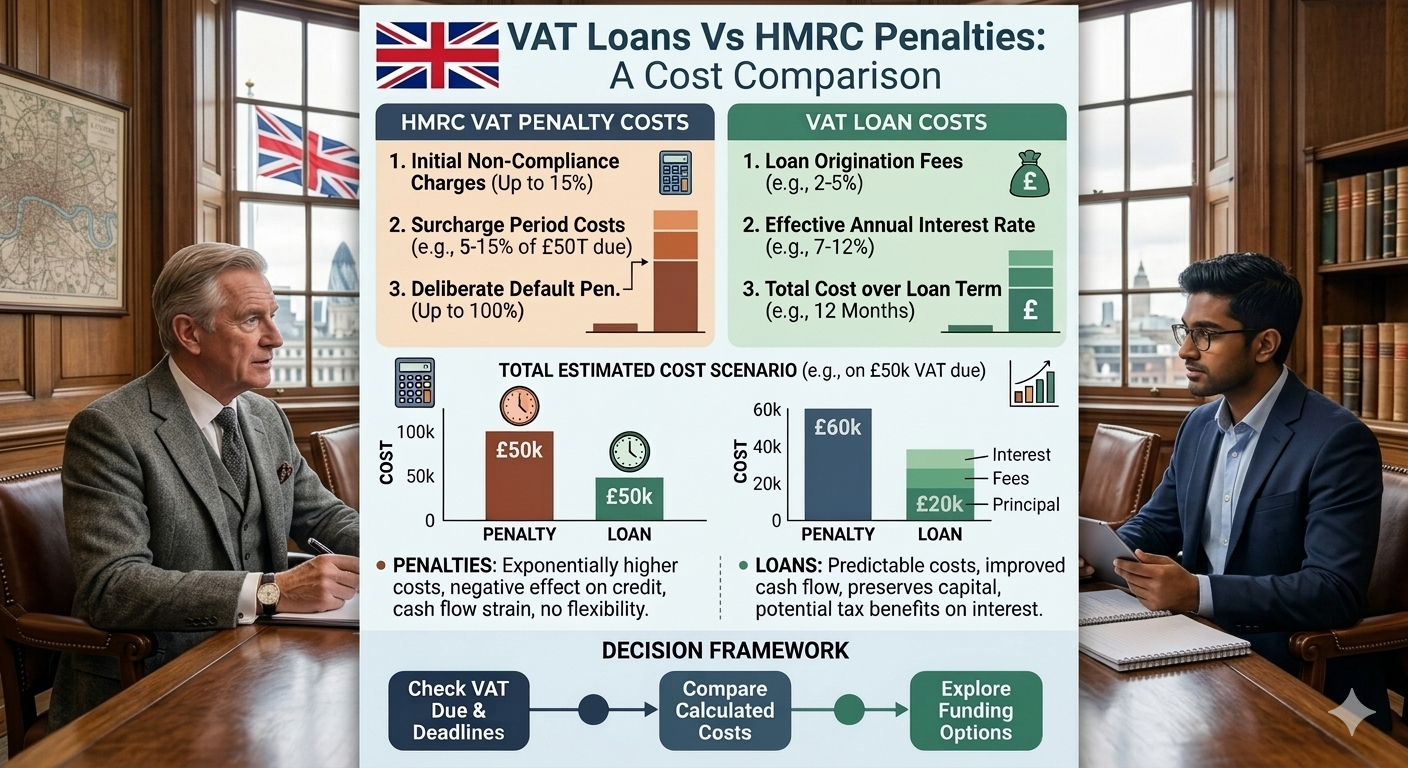

Before knowing the borrowing costs, it is important to understand the current market trends and economic scenario. Here are the recent market data:

| Factors | VAT Loans | HMRC Penalties |

|---|---|---|

| Upfront Cost | 0% - 5% arrangement fees | No upfront fees |

| Interest Rates | 6% - 20%, depending upon the lender and credit profile | HMRC late payment interest with a base rate of 2.5% |

| Penalty Charges | No charge if payments are on time | Up to 15% VAT value |

| Flexibility in Repayments | Tailored repayment plans from 3-12 months or more | Limited flexibility |

| Example of total cost (£10,000 VAT) | £10,600 – £12,000 total repayment as per the term | Up to £11,500+ (including penalties and interest amount) |

Understand the loan cost according to a general scenario of a medium-scale business.

The situation: There is a construction company that has a quarterly VAT bill of £45,000. They have accumulated some funds through a big contract, but the client is delaying and saying that it won't pay for the next 45 days. The company took a 3-month VAT loan at an interest rate of 1.5% and 1% arrangement fee.

| VAT Loan Cost | Amount |

|---|---|

| Principal Amount | £45,000 |

| Arrangement Fee | 1% |

| Total Monthly Interest | £675 per month |

| Total Amount | £47,475 |

| Monthly repayment | £15,825 |

The outcome: The company maintains £29,175 in its bank account in the first month. They can now pay staff and contractors, purchase raw materials or goods and services without any use of a costly overdraft.

VAT loans are comparatively easier to qualify for than long-term business loans. Still, lenders review your business’s financial situation, affordability and credit profile.

Here are the standard eligibility criteria:

You may be required to submit these documents:

There is usually little documentation, as business VAT loans are short-term finance with less risk.

You need loans to pay the VAT bill to HMRC. Many tailored loan options are available, but they have advantages and risks to consider.

Here are the advantages:

With the help of a loan, you spread your VAT bill over months. It means you do not need to drain your bank account all at once. It brings flexibility to manage other costs of your business.

Several VAT loan lenders in the UK provide instant decision loans. In fact, they can disburse payment within 24-48 hours.

If you pay late, it will hamper your company's financial progress and credit scores. Instead, opt for VAT loans to pay HMRC within the deadline and maintain a clean record.

As you have a loan backup, you can preserve working capital for other expenses such as wages, operating costs, new opportunities, and emergencies.

Many lenders in our panel are open to flexible repayments. They can tailor the repayments according to your cash flow.

Apart from these advantages, there are a few risks or disadvantages also involved.

Getting business loans for paying the VAT bill needs a good understanding of the lending market. The requirements and terms may differ from lender to lender. Therefore, working with the VAT loan broker minimises the risks and gives advantages like:

You get a chance to compare multiple VAT lenders operating in the UK.

With the broker’s guidance, you can easily manage the full VAT loan application process.

The broker arranges everything for you and well in time so that you can ensure accurate and timely HMRC payments.

Managing short-term glitches with the loan is possible. It means you can sit with your broker to make long-term cash flow planning.

We arrange commercial VAT loans across various sectors in the UK. These may include:

Every industry has its own mechanism of cash flow. We match them with lenders who correspond to their loan needs and credit profiles.

Are you feeling burdened due to an upcoming VAT bill? We can help. At Thebusinessfunds, we support UK business owners with independent financial advice on possible VAT loan solutions. We have a team of loan experts and accountants who do hard work in explaining every aspect of VAT finance.

Here are the reasons to choose us: