345,000 businesses closed in Q4 of 2025. Moreover, the total turnover generated by companies was £2bn less than the turnover of the businesses that shut down. And that’s not all!

Only 44%-50% of the trading businesses reveal static turnover. It highlights a troublesome business state.

Heightened global uncertainty due to the Middle East conflict and the rise in basic cost of living is the primary cause of business shutdown in 2026. Other reasons, like rising energy costs and costly manufacturing materials, also impact business growth.

Amid this, constant research is critical to “grow your small business quickly”. The eagerness to scale with the affordable funding option remains the prime aspect.

Moreover, inflation has dropped to 2.8% in May 2026. However, as economists predict, it may rise to 4% by the end of the year.

Thus, getting quick and cheap funding options may prove challenging. The interest rates have dropped on business loans. One may expect to get loans at 6%-15% for standard unsecured loans. Fewer than half (45%) of the SMEs expect to grow their headcount in 2026. It is less by 10% since 2025.

Additionally, the statement by Andrew Bailey, Bank of England governor, fuels hope.

“Recession may already be over with the economy revealing distinct signs of an upturn.”

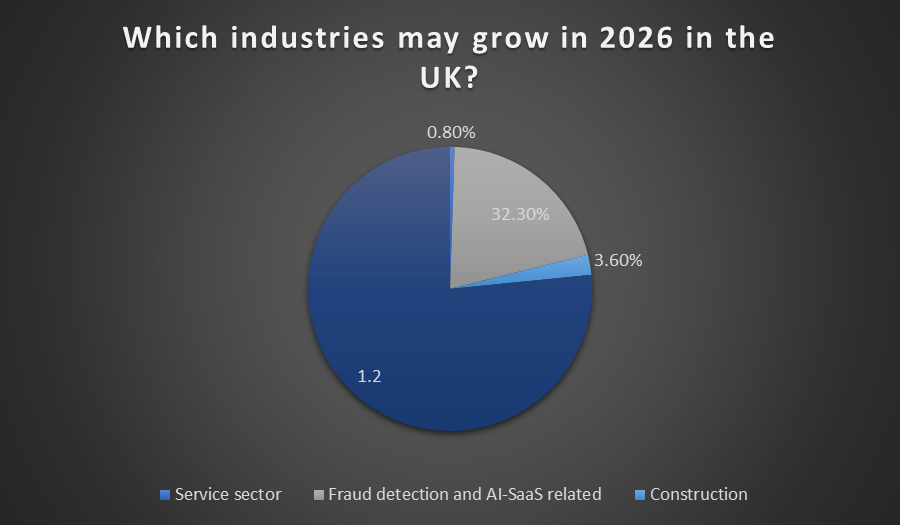

Which business industry is growing well in 2026 in the UK?

If thinking about starting a business in 2026 in the UK, AI adoption is accelerating, and consumer expectations are shifting quickly. Here are some businesses that may thrive this year:

- Service Sector industries

Service sector industries include companies that provide intangible value and deliver expertise rather than providing physical goods. For example- Restaurant, insurance, consultancy, etc. Wholesale and retail trade may grow. The largest contribution to the economy comes from the service sector (0.8%).

- Fraud detection and AI-related SAAS

The growth of fraud detection and SAAS is projected to grow by 32.3% projected revenue in 2026 for Fintech/fraud-detection and strong growth for AI-related SaaS in 2026. Thus, investing more in software development, improved behaviour analysis, identity and device verification, and cloud fraud detection services may help.

- Construction and skilled trades

The Construction industry may grow by 3.7% in 2026 in the UK. A housing shortfall of 3,00,000 homes annually means demand may stay. Moreover, with the sustainability and greenhouse awareness, over 2 million individuals want to re-construct their homes or pursue green construction and energy-friendly upgrades this year.

Moreover, the greenhouse construction market is bound to grow from 7% to 9% in 2026. Strict housing regulations, construction targets and broader residential construction drive it.

If your business deals in any of these industries, it’s high time to grow. However, entrepreneurs face strict challenges while scaling.

What primary challenges do you face in growing your small business?

According to Gravitate. digital, “Rising operating costs, inconsistent inflation, and high hiring costs are the primary challenges for business growth.” Let’s study these in detail:

- High operating costs

Energy costs, hiring costs, rent, insurance and supplier costs are rising in the UK. It may impact the bottom line and efficient business cash flow. It is high time to stress test the margins and mitigate risk early. Analyse the operations and loopholes impacting the costs.

Check which processes you can automate or eliminate to save money. Determine whether you can negotiate better supplier prices and accordingly price the services. You must inform the clients before increasing the service costs.

- Rising hiring costs

The recent changes in the employer’s National Insurance budget in 2025 have raised the cost of hiring permanently in the UK. This means that smaller employers are competing with big employers regarding salary, benefits, and flexibility.

However, the skill gap proves to be a major obstacle in hiring the best employees. It is thus high time to hire individuals with upgraded skills and outsource what you can. It may help you save money on hiring.

- Late customer payments

Late Payments drain SMEs’ cash flow. Every year, the businesses suffer a loss of £11billion. It thus provokes one to depend on high -cost borrowing and finance options to meet their business needs. You can tackle this by reducing the timelines for the final payments. Suppose you provide 20 days to clear it, slash it to 15 days. Similarly, provide early payment discounts to your loyal customers. It may help you retain clients and get payments on time.

How can you grow your business with the best funding options?

A business loan is the most popular way to finance your business needs. According to Money.co.uk, “ businesses with an annual turnover of £ 2 million saw borrowing rise by 25% compared to 2025.” They use the funds to expand, meet urgent business needs and ensure financial resilience.

Other aspects may help grow your small business swiftly in 2026.

As mentioned above, business loans are one of the easiest ways to secure quick finance. You may get up to £25000-£2 million as secured and unsecured business loans. One uses it exclusively for business purposes. You can consider secured business loans to finance a flexible amount needed when pledging an asset.

You can use a business loan for inventory updates, streamlining working capital, hiring, and business expansion.

According to a source,

” According to Hewlett-Packard, “ starting a business in the UK costs around £22,756 on average.”

The figure breaks down into the business needs, like:

| Cost category | Typical range (GBP, first year) |

| Legal fees (incorporation, contracts, IP, compliance) | £1,500 – £5,000 |

| Accounting/bookkeeping (software + accountant) | £1,200 – £3,000 |

| Payroll / HR management (software + basic HR support) | £1,000 – £3,000 |

| Licensing & permits (if applicable) | £500 – £5,000 |

| IT infrastructure (laptops, software, cloud, domain) | £1,500 – £5,000 |

| Marketing & branding (website, ads, content) | £2,000 – £10,000 |

Guarantor loans require the business owner to provide a guarantee to secure funding. It can be a family member, friend, business partner, Director, or company stakeholder.

According to Credit Connect, “businesses from manufacturing and construction industries largely depend on personal guarantees to get a loan” The personal guarantee insurance applications have also increased by 65% in Q1 2026. It is the best option for businesses operating with a poor credit history.

The qualification largely depends on the business’s affordability. The lenders conduct basic checks to analyse the borrowing potential. Thus, you may know the loan approval chances with guarantor loans with a no-credit-check facility.

The no-credit-check facility means that the credit assessment does not get recorded. Instead, it helps a business understand- approx. APR, interest costs, loan repayments, and total loan costs according to your chosen loan term. It works like a pre-qualification process that helps you know your affordability and compare the best options.

Benefits of choosing a guarantor loan for business

The primary benefits of choosing a guarantor loan for your business needs are:

- Help fetch better borrowing terms and interest rates

- Help get a higher amount than without a guarantor

- Individual businesses with a bad credit score have a high chance of loan approval

A merchant cash advance (MCA) in the UK is a lump‑sum business funding where you receive cash upfront and repay it by giving the lender a fixed percentage of your future debit and credit card sales, usually taken automatically through your card‑payment processor. It is ideal for:

- Small businesses with regular card‑payment income (e.g., shops, restaurants, salons, online retailers, service providers).

- Businesses with seasonal or fluctuating revenue that want repayments to rise when sales are high and fall when sales are low

- Firms needing fast, unsecured funding for short‑term needs (stock, refurbishment, marketing, cash‑flow gaps) rather than a long‑term loan

Who may qualify for a merchant cash advance in the UK?

- A UK‑based business (sole trader, partnership, or limited company) that has been trading for at least 6–12 months.

- Minimum monthly card turnover, often around £10,000–£20,000+, depending on the lender.

- A card‑payment provider that can share transaction data and allow automatic deductions. No traditional security or fixed‑term repayments are required. However, the cost is usually higher than a standard bank loan.

Working capital includes any business asset in liquid or tangible form. It includes aspects like- inventory and stocks, accounts receivable, prepaid expenses (insurance or rent).

You can calculate working capital using this formula:

Working capital = Current Assets-Current liabilities

You may secure working capital loans by revealing your affordability. You may qualify if:

- You have an operating history of over 6 months or a year

- You are an LLP or a limited company

- Your business is in the UK

- You have a minimum monthly turnover of £5000-£20000 or £60,000 annually

You may get a working capital loan of up to £25000 for business needs if you meet the criteria.

If you want to grow your small business by boosting the bottom line, growth capital loans may help. Capital is an important aspect of consistent business growth. Limited cash reserve, depleting one or a negligible one, impacts operations.

Startups and small businesses in the UK marketplace struggle with sustaining sound capital. Thus, it is ideal to find experts who can help boost business revenue and growth.

Growth capital loans help you fund needs like-

- Equipment purchase

- Investing in technology and software

- Paid and organic marketing efforts

- Paying existing and other debts

- Revise the business turnover

Contact brokers for business finance

Additionally, with increased business loan interest rates (6% as of January 2024), choosing the right loan is essential.

Business loan brokers help a startup or small business secure funds quickly. They do so by:

Thus, hiring an experienced business finance broker helps you save time, fetch the most affordable deal and avoid confusion. Facilities like 1:1 interaction, flexibility to adapt to changing business situations and the latest technologies quicken the loan approval process. Additionally, the brokers charge a commission fee for their services. It is separate from the repayments that one pays to a direct lender for their services.

Bottom line

These are some of the most flexible and best funding options for small business owners. If you want to grow your small business with quick funding, these may help. The most comfortable of these is contacting a business loan broker for all your business finance requirements. You may get it quickly with professional assistance.r business finance requirements. You may get it quickly with professional assistance.

Gary Weaver is a Senior Content Writer with having an experience of more than 8 years. He has the expertise in covering various aspects of business market in the UK, especially of the lending firms. As being the senior member, he contributes a lot while working at TheBusinessFunds, a reputed business loan broker.

Gary performs the major role of guiding loan aspirants according to their financing needs and also to write research based blogs for the company’s website. Previously, he has worked with many reputed business firms and therefore, he knows every nook and cranny of business financing market of the country. Gary is a post-graduate with having a degree of Masters in English language. He has also done post-graduate diploma in Business and Finance.