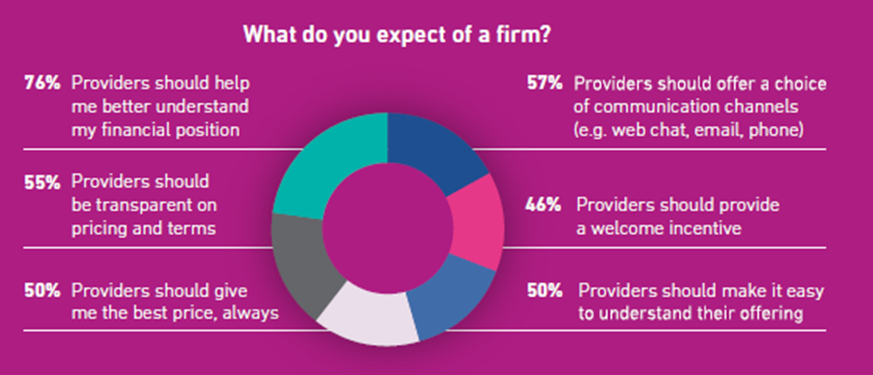

According to Experian research, “80% individual clients struggle to identify their financial needs.” They are thus willing to receive adequate guidance on that. It will help them choose the right loan product and finances.

Around 50% of clients want clear guidance on each loan product to understand the offering. Thus, helping the clients with their financial struggles improves retention. However, identifying the client’s financial problems is challenging. The businesses may benefit from the following strategies to counter the client’s financial challenges.

(Source: Experian)

How do you analyse a client’s financial needs?

Advising clients in today’s financial landscape requires more than product knowledge. It requires an accurate analysis of the financial requirements. Each client has unique requirements and struggles.

Therefore, analysing income, assets, expenditure, liabilities, and investments to gauge the affordability. It will help you provide personalised quotes according to the client’s financial requirements. Keep terms transparent for the clients to decide accurately:

- Analyse financial resilience

According to a survey, “1 in 10 individuals have no savings at all.” 21% individuals have less than 10% in savings. This thus affects one’s ability to meet the operational requirements promptly.

Thus, the loan providers must analyse financial resilience by checking aspects such as income, expenditure, profit, business stability, and emergency buffer. It will help you analyse and provide a loan that accurately meets the needs without affecting their affordability. Here are some tips that may help you:

- Map out monthly expenses and income consistency

- Determine how long they can cover basic expenses without borrowing

- Identify the pending debts and loan defaults

- Check whether they have an emergency fund

- Try to understand emotional resilience. It will help you understand the difficulties clients face in meeting the requirements/ payments.

You can use and invest in the required technologies and software for detailed research. It may help you personalise the packages for clients that fit their budgets perfectly. If low on cash, check small business loans in the UK marketplace. It may help you buy software premium packages, invest in technology and other aspects. It will help you modify the offerings accordingly.

- Segregate clients according to vulnerability

Every client is unique, and therefore, the struggles, capabilities, and resilience may vary. Segregating clients by vulnerability helps you ensure fair treatment, provide tailored support, and minimise the risk of loan default. You can segregate clients according to the following factors :

- Health: cognitive disability, mental issues, or physical impairment

- Life events: job loss, bereavement, relationship issues, leaving care

- Resilience: High debt, low income, and savings

- Capability: Low literacy and financial skills

- Identify and address the financial well-being

4 in 10 households struggle with serious financial difficulties, according to reports by Financial Fairness Tracker(2025). 93% individual households say that their bills have increased. High Council tax, water bills and energy costs were the costs individuals struggled with. Here is how you can help clients with that:

- Train your staff to spot the signs of clients’ stress sensitively

- Provide or help clients seek free and expert advice and support from MoneyHelper, National Debtline, and StepChange org.

- Help with emergency savings, understanding the credit score and managing the pending debts effortlessly.

- Provide more flexibility over payments to regular clients.

- Create a structured discovery framework

You need to follow a framework to identify the right way to approach the clients. It may vary according to the respective budget and resilience. However, understanding the basic approach may help you make it flexible accordingly.

For example, conduct the discovery call first with the potential client who’s interested in your products and services. The salesperson must be able to understand the client’s needs and check whether the offering meets their needs. If not, check how you can adjust your offerings according to the respective client’s needs.

The salesperson must operate as a trusted and most educated advisor to help the client accordingly. Apart from releasing the client’s financial worries, the person must be efficient enough to set a business rapport.

Here is the 5-step approach to creating a structured discovery framework.

- Step 1– Pre-call research – analyse customer needs before the call. Understand the pain points, needs and goals before providing the offerings.

- Step 2– identify the most effective products– Check which products may help the clients, such as an information pack or price details. Leave them with a recommendation.

- Step 3– Recap the discussion – Take notes of the discussion and discovery after the client call.

- Step 4– Decide on the time for the follow-up call: Identify the right time to conduct the follow-up call with the clients. Don’t rush it, nor delay it longer.

Accordingly, you can ask the client questions like:

- Can you meet monthly obligations?

- Do you rely on credit for essentials?

- Do you have a savings buffer?

- What are your short/long-term goals?

It will help you analyse the real client problems and operate accordingly. You can also hire experts who may help evaluate the client’s real financial concerns. Yes, that requires you to be a little financially flexible.

If you lack that, contact experts like Thebusinessfunds for help. They may help you suggest the right financial company that might help you secure the funds according to your specific goal.

- Step 5- Address debt concerns

Unless you understand the reason for the client’s debt, you cannot help them adequately. Review the financial invoices and the payment patterns of the clients. Here is how you can approach that:

- Step 1- Initiate early conversations regarding the financial situation. It should be polite and have a clear objective.

- Step 2- Try to offer flexible payments and payment options that may help the clients clear the dues promptly. It will help the clients manage the payments easily. You can also provide payment plans to help clients avoid debt.

- Step 3- Review the client’s pending payments and send reminders early. Always conduct credit and affordability scanning to analyse the client’s potential to afford the payments.

- Step 4- You can put the client’s account on hold if they miss the payments consistently.

If it does not help, you can also start charging interest on the pending dues. That’s legal and prevents the cash reserve.

Bottom line

If you struggle to identify the financial needs of your clients, these tips may help. Identify the client’s financial struggles, pains, etc. Identify how much debt they share and what approaches they follow to clear that.

Check which loan offerings may be the best given the financial obligations. Launch personalised payment plans and more payment options. It gives them more flexibility to choose the right loan and manage payments effectively.

Harry Kane is a financial writer and author who has covered wide topics related to business loans and finance for the last decade. He has been working as the Chief Contributor in finding out deals on various business finance products covered by Thebusinessfunds, a reputed business loan broker firm in the UK. The primary work of Harry is to analyse the loan requirements of various businesses according to their circumstances and affordability. He directly communicates with the loan aspirants and guides them to get the right loan matching their needs. He has a vast experience in finance writing, working with many major business firms in the UK. At Thebusinessfunds, Harry also used to write well-researched blogs covering the financial problems of business loan aspirants and providing relevant solutions. He is a postgraduate with MSc. in Banking and Finance.