Your business credit score affects loan approval, supplier terms, and contracts. Most business owners don’t check their score until it’s too late, and get turned down for something they should have easily qualified for.

A strong rating will also open up access to far better business funding solutions that are never offered to businesses with lower scores. This guide shows you proven ways to boost it in weeks.

What Is A Business Credit Score?

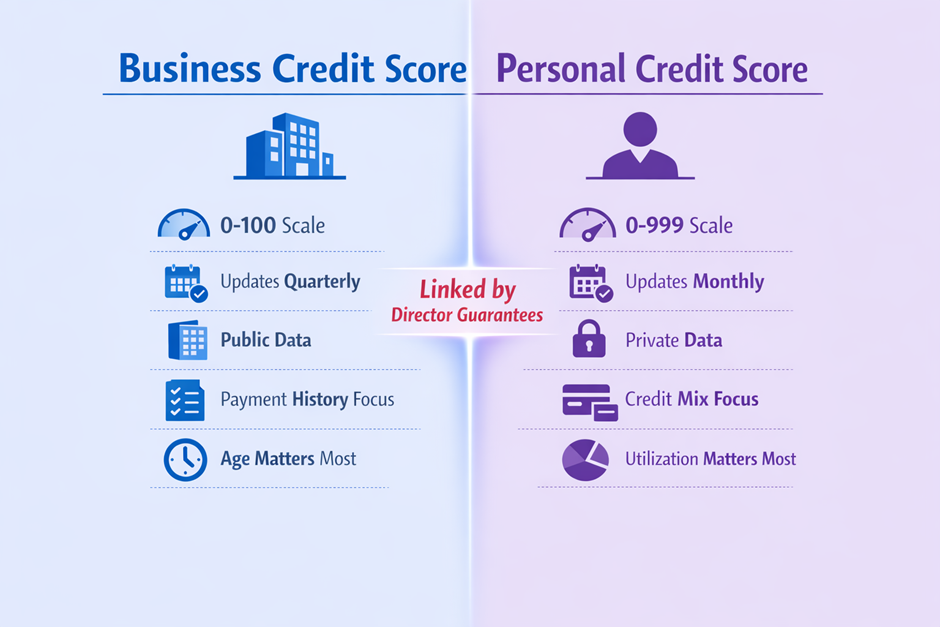

This is an entirely separate number from your personal credit score. They are held on completely separate databases. Almost all business credit agencies use a simple 0-100 scale, where over 80 is excellent, 60 is acceptable, and anything under 40 will get you declined by everyone.

It is built entirely from your company’s own behaviour, not yours as an individual. It is tied permanently to your company registration number, not your name, address or personal history.

Additional facts:

- It does not matter how much profit you make

- A £100 late payment hurts exactly as much as a £10,000 late payment

- Most agencies will not tell you when your score changes

- 90% of suppliers check your score before agreeing to terms, and almost none will tell you they did this

- A good score will usually get you better payment terms, not just approval

How To Check Your Business Credit Score?

There are both free and paid options, and for most people, the free options are more than enough 90% of the time.

Free Methods

You can view your basic filing history for free at any time on Companies House. Experian Business Express gives you a limited free snapshot of your current score once every 30 days.

You also have an absolute right under GDPR to request a full copy of your entire file from every single credit agency, for free, once every 12 months. A growing number of business bank apps now also show a basic version of your score directly inside your dashboard, with no extra charge.

If you are planning to apply for a loan, it is also worth asking business loan brokers to pull a soft search for you, which will not show up on your file at all. Most will do this for free as part of their initial enquiry. It will give you a very accurate idea of where you stand before you make any formal applications.

Paid Options

If you want ongoing monitoring and alerts when your score changes, there are a small number of paid options. Experian Business Profile Plus costs £7.99 a month and is the best value option for most small businesses.

Creditsafe monitoring starts at £50 a month, and is the service most large suppliers use themselves. Equifax sells single one-off reports for £34.99, and CreditLadder will let you add and report your own trade references from £5 a month.

What Damages Your Business Credit Score?

This is the part no credit agency will tell you clearly. Most of the things that damage your score are easy mistakes.

Late Payments

A single payment just one day over 30 days late will drop your score. A payment 60 days late will cause long-lasting damage. Any default will stay visible on your file for a full 6 years.

CCJs and Legal Action

A single CCJ will drop your score by between 30 and 50 points. It will remain on your file for 6 years, even if you pay it in full the very next day. Winding up petitions are visible to everyone.

Filing Failures

Filing your annual accounts one day late will cost you a 5 to 10 point drop. A late confirmation statement will have almost exactly the same impact. Repeated late filings will cause compounding damage.

Credit Utilisation

Using more than 75% of your available credit will drag your score down significantly. Maxing out business credit cards is one of the fastest ways to damage your score.

| Business Credit Score Ratings | |

| Score | Rating |

| 80-100 | Excellent |

| 60-79 | Good |

| 40-59 | Fair |

| 20-39 | Poor |

| 0-19 | Very Poor |

How To Improve Your Business Credit Score Fast?

The biggest myth around business credit scores is that improving them takes years. You can move your score by 20 to 30 points in 30 days.

Immediate Actions (Week 1)

First, pull all three of your credit reports and check for errors. Mistakes are extremely common, and getting one removed can add 15 points overnight. Pay any outstanding small bills under £1000. File any overdue Companies House submissions right away. Set up direct debits for every single regular payment you have.

Quick Wins (Month 1)

Start paying all of your existing suppliers two days early. Ask them explicitly to report that early payment to the credit agencies; most will do this if you ask. Keep your total credit use below 30% of your total available limit. Split any large purchases across two separate months.

30-60 Day Strategy

Open net 30 terms with at least three separate suppliers that report to the main credit agencies. Use a business credit card for every single purchase, and pay it off in full every single month. Request a credit limit increase on all your existing facilities. Then do not use any of the extra limits.

Long-Term Habits

Never miss a payment due date by even one day. File your annual accounts at least two full months before the deadline. Maintain a minimum of six weeks’ operating cash reserve in your business bank account. Build active trade accounts with at least five separate suppliers.

Special Cases: New Businesses and Recovering from Damage

All of the rules above apply to established businesses. There are separate rules for brand new companies and businesses recovering from damage.

New Businesses (Under 12 Months)

Any business less than 12 months old will not have an established credit score at all. There is no trick to get around this. For the first year, you will mostly be assessed on your personal credit score.

Open a business credit card on the day you register your company. Open three small trade accounts within the first month. Pay absolutely everything seven days early.

Recovering from CCJs

If you have an outstanding CCJ, the first thing you should do is pay it in full and request a satisfaction certificate. Once this is filed, the mark on your report will be updated to satisfy. It will still remain visible for six years, but the impact on your score will drop after 12 months.

After two years of consistent good payment history, most lenders will almost entirely ignore an old satisfied CCJ. If you have multiple CCJs, you may want to consider a voluntary arrangement to clear them.

After Company Insolvency

If your previous company was insolvent, that score will never transfer to any new company you open. Your new company will start with a completely blank score. Your personal credit may be affected depending on the circumstances of the insolvency.

Any director disqualification will remain on your record for between 2 and 15 years. You will need to use alternative forms of funding for the first 12 to 18 months of the new company.

Conclusion

The best thing about business credit scores is that they are almost entirely within your control. You do not need to wait years to fix mistakes or earn huge profits to get a great score. Most owners can add 20 to 30 points to their score inside 30 days once they know what to do. Don’t wait until you need to borrow money or open a new supplier account to check it.

FAQs

Can I check my business credit score for free?

Yes, you can check your business credit score for free. There are several providers in the UK working as special platforms to check business scores without any cost. Alternatively, you can take advantage of trial periods provided by a few agencies. In addition, you have a legal right to request a Statutory Credit Report from agencies like Experian, Equifax, and TransUnion.

Does checking my score affect it?

Checking your business credit score may not affect it. When you are checking your own score, it is usually considered a ‘soft credit check’. It is not visible to the lenders and therefore has no impact on your credit rating. However, when others check your score, and it is like a ‘hard credit check’, it will lower your score.

What is a good business credit score?

A good business credit score in the UK is generally one that keeps your company in the lower-risk category of a credit reference agency’s parameters. It is because agencies have different numerical ranges. For instance, Experian considers business scores between 80 and 100 as good or with very low risk.

Harry Kane is a financial writer and author who has covered wide topics related to business loans and finance for the last decade. He has been working as the Chief Contributor in finding out deals on various business finance products covered by Thebusinessfunds, a reputed business loan broker firm in the UK. The primary work of Harry is to analyse the loan requirements of various businesses according to their circumstances and affordability. He directly communicates with the loan aspirants and guides them to get the right loan matching their needs. He has a vast experience in finance writing, working with many major business firms in the UK. At Thebusinessfunds, Harry also used to write well-researched blogs covering the financial problems of business loan aspirants and providing relevant solutions. He is a postgraduate with MSc. in Banking and Finance.