How UK Businesses Can Qualify for a £50,000 Loan?

Businesses constantly need funds for many purposes. Business expansion, equipment purchase, marketing, research and market analysis and many more reasons.

A £50,000 business loan can fulfil a number of such requirements. But the question is how to qualify for it? Well, it should not be complicated if you know how to prepare for the loan application.

Deeper understanding makes approval decision predictable

If you once know how the loan works, its features, and the conditions to qualify, you can apply and avail funds with less effort. Staying informed is necessary for making rational and wise borrowing decisions.

Here is a guide on how to get a £50k business loan in the UK for stable, speedy business growth.

Why does a business need a loan of £50,000?

For multiple commercial purposes, a business may need this amount. A business owner may not need this amount frequently. For some significant reasons, the amount is required.

- Equipment or machinery purchase

- Employee recruitment

- Inventory purchase

- Business expansion

- New product launch

- Business debt consolidation

- Technology upgrade or software purchase

- Marketing campaign

What are the types of business loans for £50,000?

Varied loan options offer this amount with different borrowing features you can use.

| Business loan type | Suitable purpose | Features |

| Growth Capital Loans | Business growth and expansion | For business expansion, hiring, product launches. |

| Secured Business Loans | For affordable borrowing of a big amount | Includes collateral such as property, vehicles. |

| Bridging Loans | Funds to fill temporary cash flow gaps | For temporary cash flow gaps until long-term funding arrives |

| Green Business Loans | For energy-efficient business solutions | Specifically designed for environmentally-friendly business upgrades |

| Debt Financing | Working capital requirements without giving up equity | For short-term needs without compromising business ownership. |

| Merchant Cash Advance | Businesses with card transactions like hospitality and retail. | For sudden needs, repayments are collected as per a decided percentage of daily card sales |

| Professional Practice Loans | Self-employed professionals looking to expand or manage operational costs. | Offer funds for professional firms or individual professionals who run their accounting practices, law firms, dental clinics. |

Out of all the above options, the secured business loan of £50,000 and Green business loans have the lowest rates. An asset secures one. The latter one is many times supported by government support. But the other options too are affordable as they come with customised deals.

How do the £50k loans for business work?

The loans work through a clear yet simple process. If you choose after comparison, we can help you the one with fully digital application process.

- Application – Submit the financial and bank statements accurately.

- Affordability assessment – Wait for a few minutes while the lender checks your credit history, cash flow and business performance.

- Approval decision – As per the credit assessment, if the lender approves the application, receive it with the loan agreement. It has repayment terms, charges and APR.

- Fund disbursement – Read the agreement carefully and pay attention to all terms and conditions. You can ask any required questions. If satisfied, give your consent on the loan agreement.

- Monthly repayments – Repay the loan in fixed instalments. However, as per the loan type, this may change. In a merchant cash advance, you repay as per the card sales. The percentage is decided, but repayments can be smaller or bigger if the sales get volatile.

How to be eligible for £50,000 business funding?

The following conditions apply to be eligible to apply for the funding option.

- Business registration in the UK

- Minimum trading history required is 6 months to 2 years.

- Stable revenue provable through monthly turnover and cash flow

- Good credit profile. Bad credit acceptable with strong creditworthiness.

Documents required to apply for a £50,000 business loan

Be ready with the documents below. Most of the lenders demand these details.

| Document | Purpose |

| Business Bank Statements | To assess income patterns and track spending patterns |

| Profit and Loss Statements | To scrutinize profitability |

| Tax Returns | To verify earnings |

| Cash Flow Forecasts | To calculate repayment ability |

| Identification Documents | To verify business owners |

| Balance Sheets | To check assets and liabilities |

| Business Plan | To check business stability |

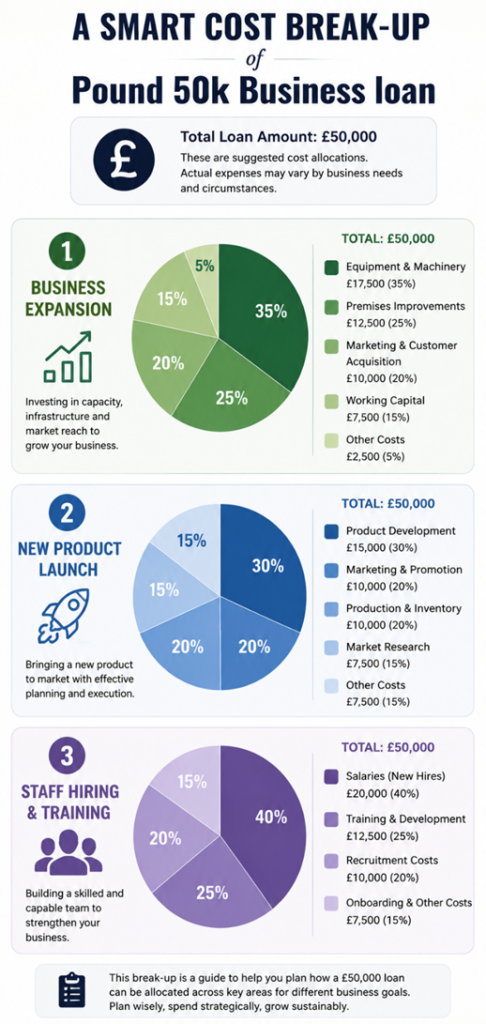

How to make the best use of £50,000?

Borrowing funds is a different thing, and using it rationally is another. How do you make sure that you will make the best use of the funds borrowed?

Here is a quick breakdown and insight into the smart ways to use the loan money. It should help you decide better.

Can a Start-up Business Apply for a £50,000 Loan?

Yes, start-ups can apply and qualify for a start-up business loan of £50,000. However, the demand for a minimum trading history and other revenue requirements should be met.

Lenders usually focus on the affordability factors below –

- Revenue projections

- Business plan

- Available collateral

- Personal finances of business owner(s)

- Industry experience

Your business plan is a significant document as it represents the overall current and future business circumstances.

How does cash flow help in loan approval?

Cash flow is the backbone of a business. It is used to handle daily operations smoothly. Especially for an unsecured £50,000 business loan, it acts as a strong affordability factor. Lenders want to know whether your business is doing fine on this aspect or not.

Signs of positive cash flow and facilitate loan approval

- Healthy account balances

- Regular customer payments

- Low missed payment history

- Controlled expenses

Warning signs of poor cash flow that cause rejection

- Large withdrawals with no explanation

- Returned payments

- Frequent use of overdraft

- Recurring short-term borrowing

Why do some businesses fail to qualify for the loan?

Certain loopholes in either application or affordability steal approval chances, making borrowing complicated.

- Poor cash flow – This is a known factor. You already know that a weakness in this part can make approval turn into rejection.

- Income/inaccurate documentation – Any of these two makes it difficult for the lender to trust your authenticity.

- Recent bad payment record – Recent six months of payment behaviour is under the scrutiny of lenders. Pay bills on time.

- Unrealistic borrowing purpose – If you fail to provide a realistic break-up of expenses, rejection may happen.

Improve creditworthiness using the ways below

- Gather financial records – Apply with the complete and accurate documents. Lenders can verify all your details online. Hence, make sure the information is consistent in all documents.

- Pay all your bills on time – That is vital if you want to prove repayment ability. Without this, no loan company is even allowed to lend you, as it is against affordability check rules.

- Check credit report for errors – Check your business credit report and make sure there are no errors. A paid bill may still be showing as pending. Get it rectified and improve your credit rating.

- Reduce pending debts – Pay off some debts, especially the expensive ones with high interest rates. It is especially advisable if you are applying for a small business loan of £50,000.

- Maintain healthy banking behaviour – Keep ample funds in your bank account, avoid frequent cash deposits, and other practices like these ensure a healthy bank statement.

The final thought…

The business finance for £50,000 in the UK can be qualified if you follow the right strategy and the lending rules. Your business repayment strength is the most important factor. Lenders need to get the loan instalments on time.

Therefore, gather all necessary details that show your income consistency. Keep the debt burden low, apply with accurate details without hiding anything and get the big amount that can support your business growth.

FAQ’s

- Can seasonal businesses qualify for a £50k business loan?

Yes, as long as the businesses can prove consistent earnings and a stable future using a strong business plan, they can qualify.

- Can I repay a £50,000 business loan early?

Yes, you can. Early repayment is allowed. However, some lenders charge for it while some don’t. Let us know your priority, and Thebusinessfunds will get you matched with the relevant lenders.

- Will applying for multiple business loans affect the business credit rating?

Yes, that certainly affects the credit rating and that too in an adverse manner. Applying to many lenders cause leave search footprint on the business credit report. This makes your business sound like a commercial entity that survives on loans only.

Lee Copper is an experienced financial content specialist helping businesses explore the UK loan market. He writes guides led by experts on business loans and finance products. His work follows strict editorial values to ensure reality, applicability, and simplicity for readers to make well-versed financial decisions. Lee creates in-depth guides backed up by research, industry best practices, and the latest market developments.